When investors pursue rental property loan approval, a well-organized rent roll often becomes one of their most persuasive tools. In the fast-moving world of real estate financing, executed lease agreements, detailed payment records, and forecasted rental income are more than just paperwork—they serve as financial proof points. Lenders want evidence of cash flow, and nothing demonstrates that more clearly than tenant history and active leases.

For those seeking quicker funding, a structured rent roll supported by lease agreements can dramatically reduce time-to-close. Understanding how to leverage this documentation can mean the difference between a stalled application and a fast-track deal.

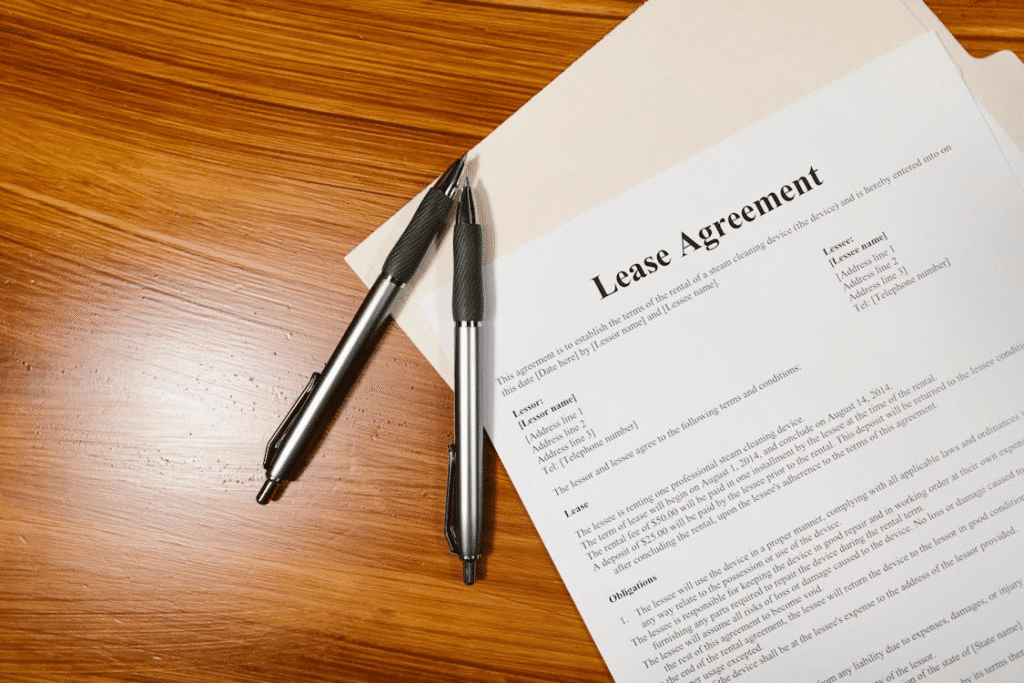

The Power of Executed Lease Agreements

One of the first documents that lenders request when evaluating rental property loan approval is the lease agreement. These contracts prove that the property is income-producing, giving lenders confidence in the investment’s viability. The strength of a loan application often hinges on how current and reliable this documentation is.

Executed leases indicate not only how many tenants are in place, but also how much rental income is committed over the coming months. Leases signed for a year or more offer greater reassurance to lenders, especially when aligned with market rates. Lenders want to see stable, predictable income, and nothing builds that case better than a lease agreement signed by paying tenants.

Moreover, leases that include escalation clauses—where rents increase annually—can help bolster projected income estimates. When included in a rent roll, such provisions show lenders that income is likely to rise, improving debt service coverage and boosting loan eligibility.

Tenant Payment Histories: Proof of Performance

Beyond signed leases, tenant payment records are a key piece of the loan evaluation process. Payment history provides hard data about tenant reliability and cash flow regularity. Lenders assessing rental property loan requirements will review whether tenants have paid on time, if there have been gaps in occupancy, and how frequently units have turned over.

A rent roll backed by 12 to 24 months of on-time payments significantly enhances a loan application. It provides reassurance that the income listed is not just theoretical but actively realized. In addition, clean records reduce the need for further verification, saving time for both investor and lender.

Tenant records should also include notes about late payments, evictions, or delinquencies. Transparency here builds trust with lenders, and minor issues—if properly explained—may not impact the outcome. Instead, presenting this data upfront shows professionalism and reduces delays during underwriting.

Projected Rent Increases and Market Comparisons

Many investors overlook the value of including projected rent increases in their rent roll presentation. When rents are currently below market value, lenders often consider the property’s income potential rather than only its current cash flow. By including realistic rent projections, investors can enhance the perceived value of the asset.

These projections should be supported by market comparables—units in the same area with similar features and higher rents. When an investor shows that existing leases can be renewed at higher rates, the lender is more likely to view the investment as appreciating. This strengthens the case for rental property investment loans, especially in rapidly growing neighborhoods.

Additionally, projected increases help when applying for refinance options or when requesting cash-out features, as they can support higher valuations during appraisal.

How a Lender-Ready Rent Roll Speeds Funding

A lender-ready rent roll isn’t just a table of numbers. It’s a detailed summary of the property’s income performance and potential. The more complete and accurate the information, the fewer questions lenders need to ask. This reduces friction and accelerates the funding process.

A comprehensive rent roll should include:

- Tenant names (initials or IDs, for privacy)

- Lease start and end dates

- Monthly rent amounts

- Security deposit information

- Payment history (preferably 12 months or more)

- Projected rent increases

- Unit status (occupied/vacant)

- Market rent estimates

When this data is clearly presented and supported by signed leases, payment logs, and market research, loan officers can evaluate the deal faster. For investors looking into private money lenders for rental property or hard money rental loans, this efficiency is especially valuable since such lenders often move quickly based on available information.

Lender-Ready Checklist for Faster Rental Property Loan Approval

Investors aiming for faster funding should prepare a lender-ready packet with the following documents:

- Executed Leases: Fully signed, dated, and current agreements for each unit.

- Tenant Payment Histories: Bank statements, ledgers, or rent collection reports showing consistent payments.

- Rent Roll Summary: One-page summary of all leases, income, and tenant status.

- Market Rent Analysis: Comparable properties supporting any projected rent increases.

- Maintenance and Repair Logs: Optional, but may support strong management and property condition claims.

- Photos or Videos of Units: Useful when dealing with rental property lenders who want visual confirmation of property quality.

- Insurance and Tax Records: Showing the property is protected and compliant.

- LLC or Ownership Documents: Verifying investor identity and legal ownership.

- Mortgage Statements (if applicable): For refinancing or assessing debt obligations.

By organizing these materials upfront, investors reduce delays caused by documentation requests. Many lenders report that delays in closing are due to incomplete or inconsistent records. A lender-ready packet puts control back in the investor’s hands.

Reducing Time-to-Close with Insula Insights

Industry professionals consistently highlight how strong lease documentation shortens funding timelines. Lease-backed rental income demonstrates property viability, reducing perceived lender risk. This can also support more competitive rental property loan rates, depending on the loan structure.

Real estate investors who maintain updated lease files and organized tenant data often experience smoother transactions. In multi-unit buildings, especially, such documentation gives lenders the clarity they need to approve funding with greater confidence.

For those working with rental property loan application processes that include multiple units, commercial elements, or mixed-use spaces, presenting this data early can prevent time-consuming back-and-forth communication.

Strengthen Your Application and Secure Faster Funding

Executed leases, reliable tenant histories, and thoughtful rent projections aren’t just background documents—they’re assets that support better deals and shorter timelines. For investors seeking rental property loan approval, a lender-ready rent roll can distinguish one application from dozens of others.

Whether applying for long-term rental loans, assessing options with rental property mortgage lenders, or exploring loans for rentals in competitive markets, preparation matters. A well-documented rent roll speaks volumes and helps lenders move quickly toward approval.

Looking for faster funding without the usual friction? Connect with Insula Capital Group to learn how streamlined rent roll preparation can open more doors for your rental property goals. Check out our loan application process.

Contact us today.